The other day I received a notice from my bank - Washington Mutual - that five debits had not cleared my account and therefore I was charged $30 per transaction for the overdraw - a total of $150. I discovered the problem when I was glancing at my accounts for another reason, before I got a notice from the bank.

I made a mistake. I have two checking accounts there and each has a debit card. Somehow the card I normally use had gotten shoved down in my wallet and the other one, which I normally do not use, was staring out at me. I used the wrong card for those transactions and therefore overdrew that account.

I wrote to the bank to ask

1) why don't they let me know the day the overdraw occurs, and

2) how about reversing some of those charges.

They wrote back. Sorry can't reverse the charges. For my convenience they did overdraw the account rather than bounce the checks.

I wrote back. What about my first question? And why are your fees so ridiculously high?

The answer: WaMu does offer the option of sending alerts. The message went on to describe how to set it up to get alerts. Fees are always being reviewed to be competitive with the industry.

Of course I already get alerts. Just not in time. And fees being set to be competitive? How about setting them to draw customers or keep the ones you have? The messages clearly were standardized. I guess the person answering picks out a couple of key words and sends the appropriate response.

In other words, I got no satisfaction. My daughter Elaine mentioned that she is looking into getting a credit union account instead because of the ridiculous fees and the delays in clearing checks whenever she and her husband deposit a large check.

I am now in the midst of choosing a credit union myself. What I hope to find is one that offers the options I find most valuable - free billpay, for example - as well as better rates for savings and lower fees for everything. My first step was to go to bankrate.com.

Bankrate.com offers a page: Six ways to find a credit union. For me, the big find on this page was CUNA: The Credit Union National Association.

On this site I found a page that helps one find a credit union. Because I am not employed right now and do not belong to any organizations (other than animal rights and eco types) or to any church, I simply entered my city, county, and state. Five matches turned up. I am now set to evaluate those matches.

Friday, March 28, 2008

Saturday, March 22, 2008

Freakonomics, by Steven Levitt and Stephen Dubner

Levitt and Dubner repeatedly say that this book does not have a "theme". And in the sense that Blink or The Tipping Point have themes, they are right. But it does have a fundamental focus: on "conventional wisdom".

Levitt, as an economist, has made his name by asking different questions - like "do teachers cheat?" - and by finding ways to sort data to get the answers he is looking for. Dubner interviewed Levitt for a NYT article a while back and soon a collaboration was born - the collaboration that yielded this book. Both Levitt and Dubner appear to be good writers, as evidenced by the Freakonomics blog at http://freakonomics.blogs.nytimes.com/, where both post individual as well as joint articles. I sense that the overall style of the book is more Dubner than Levitt, based on my seeing Dubner speak at Prosper Days (see my articles on Prosper Days at http://fightdebt.blogspot.com/search/label/Prosper%20Days).

In this book we find answers to a wide range of questions that few people would think to ask, about topics from sumo wrestlers to parenting. What does it have to do with economics? Simply that it has to do with how people get what they want - and how people can be encouraged to do the right thing and avoid doing the wrong thing. The outline of the entire book can be found in Dubner's original article, which is included as part of the additional material in this book, along with selected blog posts and heavy-duty footnotes.

I for one really did want a bit more of a theme than this non-theme, but I do think the basic premise is sound and a good reason for people to read the book - it is important to question conventional wisdom. For example, at one point another economist read Levitt's original article on the relationship between abortion and the drop in crime, and he said (I'm paraphrasing), "I have read this over and over and I can't find anything wrong with it, but I still don't believe it.". This is how most of us are: we can be faced with incontrovertible evidence but we find it difficult to let go of what we have believed for so long.

Portfolios: Prosper vs Lending Club

*edited 3/26/08

I recently joined Lending Club and added $500 to my account. I received an incentive deposit of $50 - I think because I joined through someone else's link. (You too can get an incentive when you join - click on the link to the right.)

Today I created a portfolio on Lending Club. I have six portfolios on Prosper. Here is a quick comparison of the two:

Lending Club:

There are actually two types of portfolios on Lending Club. The notes below apply to the automatic portfolio, known as LendingMatch. The other type is formed when you choose individual loans.

Prosper:

What then?

On Prosper, it takes several minutes before a portfolio chooses loans that meet the criteria. On Lendingclub a list of loans is chosen immediately and you can select some from the list to delete if you like. (On Prosper you can't withdraw from a bid that is placed automatically by your portfolio.)

It takes less time, then, to set up a Lending Club portfolio and you get immediate results. On Prosper, though, you can add more criteria to tailor the loans you make. What works best for you obviously depends on your goals and preferences.

I recently joined Lending Club and added $500 to my account. I received an incentive deposit of $50 - I think because I joined through someone else's link. (You too can get an incentive when you join - click on the link to the right.)

Today I created a portfolio on Lending Club. I have six portfolios on Prosper. Here is a quick comparison of the two:

Lending Club:

There are actually two types of portfolios on Lending Club. The notes below apply to the automatic portfolio, known as LendingMatch. The other type is formed when you choose individual loans.

- $500 minimum for each portfolio

- Choice of "risk levels" from low to high but no other options

- $25 bids on each loan are automatically set - that is, the portfolio automatically bids $25 on each loan that fits the criteria. You can change the amount of each bid when you "review" the portfolio.

Prosper:

- No minimum for each portfolio

- Wide range of options in addition to risk levels. Can choose to exclude "auto funding", can set no. of delinquencies that are acceptable, can choose to include only those loans that friends of the borrower have bid on, for example.

- You choose the minimum bid ($50 or more).

What then?

On Prosper, it takes several minutes before a portfolio chooses loans that meet the criteria. On Lendingclub a list of loans is chosen immediately and you can select some from the list to delete if you like. (On Prosper you can't withdraw from a bid that is placed automatically by your portfolio.)

It takes less time, then, to set up a Lending Club portfolio and you get immediate results. On Prosper, though, you can add more criteria to tailor the loans you make. What works best for you obviously depends on your goals and preferences.

Friday, March 7, 2008

Lending Club

At Prosper Days I learned of a couple of other new "peer-to-peer" lending companies. One is loanio, which has not yet gone live. Another is Lending Club. I just joined Lending Club, in part as a diversification strategy and in part to find out what it's like.

Lending Club is similar to Prosper in its overall makeup: people lend to other people. Specifically, Lending Club makes loans and sells them to individual lenders, just like Prosper. There are, of course, differences. Lending Club only accepts borrowers with credit scores of 640 or higher, and may reject those if their credit balances are too high.

Acceptance as a lender is also similar to Prosper, except that instead of a checking account a lender can wire money to Lending Club. There aren't other options, like credit cards, yet.

Borrowers and lenders pay fees to Lending Club, based on the value of the loan. My quick glance tells me the percentages are higher than Prosper's.

Lending Club offers portfolios too, although some of the criteria differ from Prosper's.

I will offer more details in future posts.

Sunday, March 2, 2008

Stephen Dubner: Unexpected consequences

The keynote speaker on the second day of Prosper Days was Stephen Dubner, co-author (with Steven Leavitt) of Freakonomics: A Rogue Economist Explores the Hidden Side of Everything, author of Turbulent Souls: A Catholic Son's Return to His Jewish Family, Confessions of a Hero-Worshipper, and a children's book. Obviously it was Freakonomics that brought Dubner into the Prosper fold. Or at least to the podium. He connected his work to Prosper members by describing research on altruism, picking up on the "people helping people" theme.

Dubner is a likeable, funny guy, and an excellent speaker. He's clearly been at this for some time. In his presentation for Prosper Days he focused on the same general topic, the overarching topic, of Freakonomics: the study of incentives, but zeroed in particularly on the quality of research and how that quality reflects (poorly or well) real life.

Scrutiny tweaks the outcome. For example, there is a difference between "stated preferences" and "revealed preferences". If the people in a room are asked to raise their hands if they wash their hands after using a public toilet close to 100% will raise their hands. If, instead, researchers slyly count the number of persons washing their hands after using a public toilet they find that about 30% do not. This difference obviously comes from a factor known as "scrutiny".

What are the rewards, Dubner asks, for truthfulness? What is the cost of dishonesty? These are the questions that bring us a true understanding of incentives.

Gaming the Altruists . Dubner applauded the Prosper crowd for its apparent altruism. He then launched into the research on altruism in humans, taking us from "conventional wisdom" that says humans are innately altruistic (I am not sure how conventional that wisdom is, myself; I do not think humans are innately altruistic and don't know that I ever have) through the "Dictator Game" and beyond, to conclusions that, surprise surprise, vary with the rules of the game - the way the research is designed.

Who done it. The results of a research project are also affected by the person(s) doing the research. That is, the persons who interact with the research subjects. It turns out that no matter how well-designed the project is, the greatest cooperation will be obtained when requested by blonde women. I guess we all knew that already, though, didn't we?

Unassuming. Dubner kept coming back to the questions we ask and those we don't. Sometimes we have to ask questions in different ways at different times to separate ourselves from our own assumptions. Sometimes we don't think to ask the simple questions.

All of these elements affect the value of research. It's a mistake to rely upon research until you have reviewed how it was done and by whom.

Dubner's speech drew upon elements of the next book he and Leavitt plan to publish in about a year. Throughout his talk he referred to works by others, notably Predictably Irrational: The Hidden Forces that Shape Our Decisions, by Dan Ariely. Dubner's message, overall, was to question not only authority but also conventional wisdom when trying to predict the behavior of others or, for that matter, ourselves. We don't always or even often behave rationally. Perhaps by knowing some of the motives behind our own behavior we can prevent ourselves from making serious mistakes.

Dubner is a likeable, funny guy, and an excellent speaker. He's clearly been at this for some time. In his presentation for Prosper Days he focused on the same general topic, the overarching topic, of Freakonomics: the study of incentives, but zeroed in particularly on the quality of research and how that quality reflects (poorly or well) real life.

Scrutiny tweaks the outcome. For example, there is a difference between "stated preferences" and "revealed preferences". If the people in a room are asked to raise their hands if they wash their hands after using a public toilet close to 100% will raise their hands. If, instead, researchers slyly count the number of persons washing their hands after using a public toilet they find that about 30% do not. This difference obviously comes from a factor known as "scrutiny".

What are the rewards, Dubner asks, for truthfulness? What is the cost of dishonesty? These are the questions that bring us a true understanding of incentives.

Gaming the Altruists . Dubner applauded the Prosper crowd for its apparent altruism. He then launched into the research on altruism in humans, taking us from "conventional wisdom" that says humans are innately altruistic (I am not sure how conventional that wisdom is, myself; I do not think humans are innately altruistic and don't know that I ever have) through the "Dictator Game" and beyond, to conclusions that, surprise surprise, vary with the rules of the game - the way the research is designed.

Who done it. The results of a research project are also affected by the person(s) doing the research. That is, the persons who interact with the research subjects. It turns out that no matter how well-designed the project is, the greatest cooperation will be obtained when requested by blonde women. I guess we all knew that already, though, didn't we?

Unassuming. Dubner kept coming back to the questions we ask and those we don't. Sometimes we have to ask questions in different ways at different times to separate ourselves from our own assumptions. Sometimes we don't think to ask the simple questions.

All of these elements affect the value of research. It's a mistake to rely upon research until you have reviewed how it was done and by whom.

Dubner's speech drew upon elements of the next book he and Leavitt plan to publish in about a year. Throughout his talk he referred to works by others, notably Predictably Irrational: The Hidden Forces that Shape Our Decisions, by Dan Ariely. Dubner's message, overall, was to question not only authority but also conventional wisdom when trying to predict the behavior of others or, for that matter, ourselves. We don't always or even often behave rationally. Perhaps by knowing some of the motives behind our own behavior we can prevent ourselves from making serious mistakes.

Saturday, March 1, 2008

Prosper transparency

Another apparent theme at the Prosper Days conference was "transparency" - the term that has come to mean a willingness to share the guts of an operation openly. Prosper's most obvious claim to transparency is the availability of its programming and data. By making this resource available to third parties, Prosper expands its own visibility. Several developers have taken advantage and are offering different ways of viewing and using the data.

Software engineer Eric Petroelje

Eric was tapped as panel leader or member more than once at Prosper Days. His expertise in software development allowed him to take advantage of the Prosper API (application programming interface) to indulge his other passion: investing in stock and real estate as well as Prosper lending. Eric created ericscc.com (Eric's Credit Community), a source of market information and lending statistics for lenders, and fantasy prosper, a market simulation tool for lenders. Tools like Eric's give investors additional information on how Prosper is doing in general as well as information on individual lenders and borrowers (not by real name but by Prosper member name). I was able to look up the difference between the number of bids I make and the number I win, for example. I just noticed that Eric has posted a list of the 25 borrowers with the greatest number of endorsements. It might be a good idea for me to use this list for bidding.

Carnegie Mellon Professor Doctor Robert Hampshire

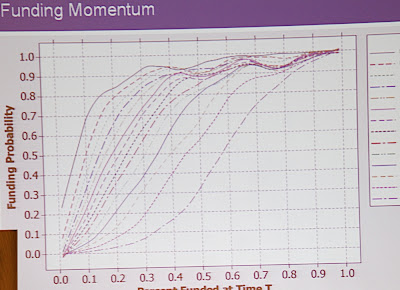

Dr. Hampshire offered a glimpse of the academic uses of Prosper data. He is leading a team, including a doctoral candidate we met the first day, in developing statistics on Prosper lenders. He offered some glimpses at the results so far, in the form of charts.

This chart shows the "tipping point" when a loan is expected to "go all the way". When bids on loans are tracked through time, those that reach 40% of funding tend to go all the way to 100%. In other words, when lenders see that a loan is 40% funded they are likely to bid on that loan and bring it all the way up.

Chief technology Officer and Co-Founder John Witchel and Chief Financial Officer Kirk Inglis

At most or all of the sessions, Prosper executives hung out at the rear of the room. They spoke up if someone on a panel gave out the wrong information and they readily answered questions. Prosper members are not a lightweight group - I don't think most of us would do this sort of thing if we didn't have the guts to take a chance on an idea - and often members would ask pointed questions that revealed more about the company than the presentations did. I was pleased to see how easily and openly Prosper executives fielded the questions. I think the reason they did not have to hesitate or obfuscate is that they rely on member experiences, questions, and recommendations to improve the way Prosper works.

I have attended many conferences for many different reasons over the years. The transparency of this company really stood out in my mind.

Software engineer Eric Petroelje

Eric was tapped as panel leader or member more than once at Prosper Days. His expertise in software development allowed him to take advantage of the Prosper API (application programming interface) to indulge his other passion: investing in stock and real estate as well as Prosper lending. Eric created ericscc.com (Eric's Credit Community), a source of market information and lending statistics for lenders, and fantasy prosper, a market simulation tool for lenders. Tools like Eric's give investors additional information on how Prosper is doing in general as well as information on individual lenders and borrowers (not by real name but by Prosper member name). I was able to look up the difference between the number of bids I make and the number I win, for example. I just noticed that Eric has posted a list of the 25 borrowers with the greatest number of endorsements. It might be a good idea for me to use this list for bidding.

Carnegie Mellon Professor Doctor Robert Hampshire

Dr. Hampshire offered a glimpse of the academic uses of Prosper data. He is leading a team, including a doctoral candidate we met the first day, in developing statistics on Prosper lenders. He offered some glimpses at the results so far, in the form of charts.

This chart shows the "tipping point" when a loan is expected to "go all the way". When bids on loans are tracked through time, those that reach 40% of funding tend to go all the way to 100%. In other words, when lenders see that a loan is 40% funded they are likely to bid on that loan and bring it all the way up.

Chief technology Officer and Co-Founder John Witchel and Chief Financial Officer Kirk Inglis

At most or all of the sessions, Prosper executives hung out at the rear of the room. They spoke up if someone on a panel gave out the wrong information and they readily answered questions. Prosper members are not a lightweight group - I don't think most of us would do this sort of thing if we didn't have the guts to take a chance on an idea - and often members would ask pointed questions that revealed more about the company than the presentations did. I was pleased to see how easily and openly Prosper executives fielded the questions. I think the reason they did not have to hesitate or obfuscate is that they rely on member experiences, questions, and recommendations to improve the way Prosper works.

I have attended many conferences for many different reasons over the years. The transparency of this company really stood out in my mind.

Subscribe to:

Posts (Atom)